Understanding the De-dollarization Debate

Never before has the "de-dollarization" narrative commanded such widespread attention across global media, policy circles, and financial markets. Yet this surge in coverage has revealed a troubling phenomenon: vastly different outlets present dramatically contradictory assessments of the same underlying trends. Some proclaim the dollar's imminent collapse, while others dismiss de-dollarization as overblown rhetoric.

To understand these disparities, we analysed 190 sources across multiple metrics like: absolutist terminology (measuring dramatic language), predictions of USD decline (tracking specific forecasts and timelines), and our propaganda risk index, a composite measure combining emotional language, empirical evidence, and citation quality.

Beyond the quantitative analysis, we reviewed the actual content of these articles to identify what's driving the divergent narratives and separate the underlying realities from the rhetorical positioning.

Table 1: Media Categories and De-dollarization Coverage Quality

Rating Methodology

- Absolutist Terminology (1 = cautious/conditional, 5 = highly absolutist and dramatic)

- Speed of USD Decline (1 = vague/long-term, 5 = imminent or underway)

- Tone Toward the U.S. (1 = strongly negative, 5 = strongly positive)

- Emotional vs. Neutral Language (1 = highly emotional or alarmist, 5 = completely neutral and analytical)

- Empirical Evidence (1 = none or anecdotal, 5 = well-sourced, well-integrated data)

- Citation Quality (1 = vague/unverifiable sources, 5 = multiple reputable and diverse citations)

- Propaganda Risk Index: (Emotional Language + Empirical Evidence + Citation Quality) / 3 (the lower the score the more likely propaganda)

The Propaganda Risk Framework

Our propaganda risk index identifies three distinct reporting clusters:

High Risk (1.0-2.5): Dominated by Russian and Iranian state media, characterised by dramatic claims with minimal supporting data.

Moderate Risk (2.5-3.5): Including Chinese media and some cryptocurrency publications, mixing legitimate analysis with ideological positioning.

Low Risk (3.5-5.0): Academic sources, financial institutions, and quality mainstream media, grounding analysis in verifiable data.

Current State of Dollar Dominance

A clear pattern emerges from the scoring: sources from countries under US sanctions or in geopolitical competition with America consistently employ more dramatic language while providing less empirical evidence.

However, before examining these trends, let’s establish a baseline from some of the most credible sources.

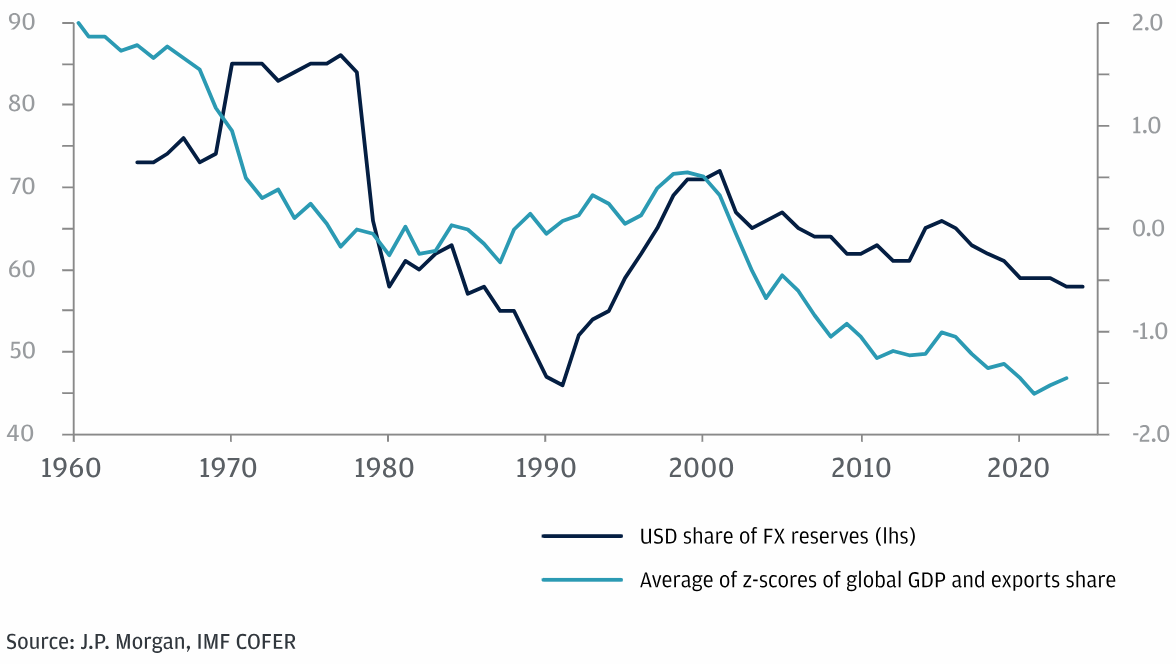

According to J.P. Morgan's comprehensive analysis, the US dollar maintained its position in 88% of all foreign exchange transactions as of 2022, which is near historical highs. The Chinese yuan, despite significant growth in recent years, accounted for just 7% of transactions.¹

The International Monetary Fund also confirms that while the dollar's share of global reserves has declined from approximately 70% in 2000 to 59% today, this represents gradual rebalancing rather than collapse.²

As Robert Wade from the London School of Economics notes in his analysis: "Dollar dominance will surely end – but not in the foreseeable future. Most of the world has no prospect of an alternative to the international dollar to be used at scale in the next two decades or so".³

This measured assessment contrasts sharply with claims from less credible sources. Tasnim News Agency, for instance, declared that "The Eurasian Economic Union's de-dollarization process has almost been completed"4 – a statement that refers only to internal trade between the Eurasian Economic Union, representing a fraction of global commerce.

Comparing Categories: How Different Outlets Frame De-dollarization

Academic vs Russian Media: The Credibility Chasm

The starkest contrast in our dataset emerges when we compare academic institutions with Russian state media.

Academic institutions represent the gold standard in our analysis, with a propaganda risk score of 4.56, while Russian outlets score a concerning 1.85. Their approach emphasizes long-term structural analysis, scoring just 1.92 on the speed of USD decline – the lowest across all categories. With citation quality at 4.92 and empirical evidence at 4.38, academic sources ground their analysis in verifiable research.

Russian media presents the opposite profile. With absolutist terminology at 3.63 and speed of decline at 3.88, they predict imminent dollar collapse. Their emotional language score of 2.00 reveals heavy use of inflammatory rhetoric, while their empirical evidence score of 1.69 – the lowest in our dataset – exposes the absence of supporting data.

Banks / Economic Institutions vs Iranian Media: Professional vs Propaganda

Banks and economic institutions demonstrate measured analysis with an average propaganda risk of 4.07. Financial institutions acknowledge real trends while maintaining perspective. Their average "Speed of USD Decline" score of 2.21 suggests gradual, decades-long transitions. They score 4.18 on emotional vs neutral language, indicating professional, dispassionate analysis. Most importantly, their empirical evidence score of 3.93 shows reliance on concrete data.

Iranian media, by contrast, scored 2.15 on propaganda risk. Their absolutist terminology score of 3.55 and speed of decline at 3.80 reveal dramatic predictions unsupported by their empirical evidence score of just 1.95. The “tone towards the US score” of 1.85 – indicating strong negativity – suggests political rather than economic motivations drive their coverage.

Crypto Media vs General Media: The Alternative Perspective Divide

Cryptocurrency media presents an interesting middle ground with a propaganda risk score of 3.56. Their coverage splits between legitimate blockchain innovation discussion and ideological promotion of dollar alternatives. With empirical evidence at 3.41, they provide more substantiation than state media but less than traditional financial sources.

The "Media-Other" category, encompassing diverse alternative outlets, scores 3.44 on propaganda risk. This category includes both rigorous independent analysis and ideologically-driven content, creating wide variation within the group. Their tone towards the US score of 2.95 suggests moderate criticism rather than outright hostility.

Meta-Analysis of All Sources

Specific Media Analysis: Four Detailed Case Studies

Case Study 1: RT versus Reuters – The Extremes of Coverage

The contrast between RT (Russia Today) and Reuters exemplifies the full spectrum of de-dollarization reporting quality.

RT's Systematic Bias:

- Absolutist Terminology: 3.67

- Speed of USD Decline: 4.00

- Emotional vs Neutral Language: 1.67

- Tone Toward US: 1.33

- Empirical Evidence: 1.33

- Citation Quality: 1.67

- Propaganda Risk Index: 1.67

RT's coverage relies heavily on official statements and selective statistics. Articles feature dramatic quotes from Russian officials claiming de-dollarization is "vital" and "accelerating," but provide minimal contextual data or independent verification. Their reporting consistently omits contradictory evidence, such as the continued dominance of dollar-denominated trade globally.

Reuters' Professional Standards:

- Absolutist Terminology: 2.00

- Speed of USD Decline: 2.00

- Emotional vs Neutral Language: 4.50

- Tone Toward US: 3.50

- Empirical Evidence: 4.50

- Citation Quality: 4.80

- Propaganda Risk Index: 4.53

Reuters maintains rigorous journalistic standards, acknowledging de-dollarization initiatives while providing essential context. Their reporting consistently notes that despite various initiatives, "the US dollar held as reserves is higher than all the other currencies combined." They cite multiple sources, present opposing viewpoints, and distinguish between bilateral arrangements and systemic change.

Case Study 2: Global Times versus Geopolitical Economy Report

Global Times (Chinese state media):

- Absolutist Terminology: 3.20

- Speed of USD Decline: 3.40

- Emotional vs Neutral Language: 3.00

- Tone Toward US: 2.40

- Empirical Evidence: 2.80

- Citation Quality: 3.00

- Propaganda Risk Index: 2.87

Global Times takes a notably more moderate approach than Russian outlets. They frame de-dollarization as "diversification" rather than replacement, reflecting China's complex position as both a challenger to US hegemony and a major holder of dollar assets. There isn’t a huge amount of supporting data to be found in the reporting, and some headlines are dramatic, but their coverage emphasises gradual transition and "win-win cooperation" rather than pure confrontation.

Geopolitical Economy Report:

- Absolutist Terminology: 3.50

- Speed of USD Decline: 3.75

- Emotional vs Neutral Language: 2.50

- Tone Toward US: 2.00

- Empirical Evidence: 3.25

- Citation Quality: 3.50

- Propaganda Risk Index: 3.08

This alternative media outlet, despite its Western origin, shows strong anti-establishment bias. Their coverage emphasizes US weaponisation of the dollar and presents de-dollarization as inevitable justice. However, they provide more empirical support than state media, citing Federal Reserve data and bank analyses, though often selectively to support predetermined narratives.

Case Study 3: Cryptocurrency Media's Divided Coverage

The cryptocurrency media sector reveals fascinating internal divisions about de-dollarization.

ZeroHedge (Tyler Durden's analysis):

- Absolutist Terminology: 2.50

- Speed of USD Decline: 3.00

- Emotional vs Neutral Language: 3.50

- Tone Toward US: 2.50

- Empirical Evidence: 4.20

- Citation Quality: 4.50

- Propaganda Risk Index: 4.23

ZeroHedge surprises with relatively robust sourcing, quoting things like Deutsche Bank analysts and providing concrete data about bond market dynamics.

Even if the language is sometimes dramatic, the article acknowledges various factors: "Persistent fiscal indiscipline, rising debt-to-GDP ratios, erratic policy shifts… erode the confidence that anchors reserve currency status. If that erosion continues, the dollar may eventually cede ground... but through the gradual accumulation of self-inflicted wounds. In the meantime, the world remains tethered to King Dollar".5

Generic Crypto Outlets (Average):

- Absolutist Terminology: 3.12

- Speed of USD Decline: 3.38

- Emotional vs Neutral Language: 2.88

- Tone Toward US: 2.75

- Empirical Evidence: 2.50

- Citation Quality: 2.75

- Propaganda Risk Index: 2.71

Other crypto outlets score significantly lower, often conflating de-dollarization with wider cryptocurrency adoption. They provide limited empirical evidence while making strong predictions about digital currencies replacing traditional finance.

Case Study 4: Newsweek versus Mehr News Agency

Newsweek:

- Absolutist Terminology: 3.50

- Speed of USD Decline: 2.50

- Emotional vs Neutral Language: 3.00

- Tone Toward US: 3.50

- Empirical Evidence: 2.50

- Citation Quality: 3.00

- Propaganda Risk Index: 2.83

Newsweek's coverage of Trump's threats to BRICS nations demonstrates that sensationalist language isn't exclusive to non-Western media. Their article "Donald Trump Warns BRICS Over Dollar Move: 'Go Find Another Sucker Nation'"6 relies heavily on inflammatory quotes without substantial economic analysis, showing how even mainstream Western outlets can prioritise drama over substance.

Mehr News Agency (Iran):

- Absolutist Terminology: 3.80

- Speed of USD Decline: 4.00

- Emotional vs Neutral Language: 1.80

- Tone Toward US: 1.50

- Empirical Evidence: 1.50

- Citation Quality: 1.80

- Propaganda Risk Index: 1.77

Iranian coverage treats de-dollarization as both inevitable and imminent, with minimal supporting evidence beyond official government statements. Their reporting frames dollar dominance as a tool of oppression requiring immediate resistance.

Key Drivers of De-dollarization: Evidence-Based Analysis

1. Financial Weaponisation and Sanctions Risk

The most significant catalyst for de-dollarization efforts isn't economic theory but geopolitical risk. As Robert Wade observes: "The US took weaponization to a new level when it used the dollar payments system to freeze Russia's access to $300 billion in liquid foreign exchange reserves in the wake of Russia's invasion of Ukraine in February 2022".3

This assessment finds support across credible sources. RBC Wealth Management confirms: "Countries that face restrictions over the use of this system due to sanctions would like to see an alternative... The freezing of Russia's dollar reserves and exclusion from the SWIFT system also put countries on notice that they might be next".2

The Takshashila Institute's analysis adds crucial context: "Many developing countries, including traditional US allies such as Saudi Arabia, have begun to fear that, should they ever find themselves on the opposite side of the US in a geopolitical dispute, their dollar-denominated assets will not be safe".7

Concrete responses to sanctions risk include:

- Russia reducing US Treasury holdings from $96.1 billion to $14.9 billion in just two months (March-May 2018)

- China and Saudi Arabia establishing currency swap agreements worth billions

- ASEAN countries developing frameworks for local currency trade settlement

The Cambridge Elements research provides essential perspective: "While Russia may be a unique strategic adversary, its behavior reminds one of former US Treasury Secretary Jack Lew's warning in 2016 that 'the more we condition the use of the dollar and our financial system on adherence to US foreign policy, the more the risk of migration to other currencies and other financial systems in the medium-term grows'".8

2. Structural Economic Shifts

The expansion of BRICS to include Saudi Arabia, Iran, and the UAE represents a genuine structural shift in global economics. The Tricontinental analysis by Gao Bai notes that "BRICS accounts for 24 percent of world GDP and over 16 percent of world trade".9

Yet the Cambridge Elements research provides crucial balance: "The emerging BRICS de-dollarization infrastructure does not yet allow the BRICS members to make a complete break from the existing US dollar-based financial system... BRICS de-dollarization initiatives are predominantly happening at the sub-BRICS level and have not achieved the necessary economies of scale".8

China's Cross-Border Interbank Payment System (CIPS) illustrates both progress and limitations:

- Daily processing reached RMB135.7 billion by end-2020

- 1,159 indirect participants across 85 countries

- But still represents a fraction of SWIFT's $5 trillion daily volume

As the Responsible Statecraft analysis notes: "It is worth remembering two points. First, creating a widely used international currency is bound to take decades. It took four to five decades from when the US surpassed Britain as a global economic power in the late nineteenth century to when it became the dominant financial power".10

3. Interest Rate Dynamics and Economic Fundamentals

An underreported factor in de-dollarization is pure economics rather than geopolitics. The Geopolitical Economy analysis notes: "For the first time in 20 years, it is cheaper to borrow short term in RMB compared to USD. One Year T-bill rates indicate that borrowing in RMB is 2% points cheaper than USD".11

This isn't ideological but practical. When the Federal Reserve raised rates to combat inflation, dollar financing became more expensive, naturally pushing traders toward alternatives. As RBC Wealth Management observes: "This flip in relative cost of borrowing happened independently, but around the same time as the Russian invasion. Some part of the switch away from dollar was disproportionately attributed to the sanctions, while the interest rate factor was underestimated".2

The J.P. Morgan analysis provides crucial context about currency cycles: "The start of a new dollar bear market? Too early to say... The dollar has experienced four distinct cycles averaging 9 years in length with moves of the order of 40% to 60%".1

The Reality of BRICS Financial Infrastructure

Development Finance: The New Development Bank

The BRICS New Development Bank (NDB) represents the most concrete de-dollarization achievement. As detailed in the Cambridge analysis: "By the end of 2019, cumulative approved local currency loans represented 27 percent of the NDB's total portfolio... This number is remarkable because it is higher than the local currency loan percentages of other major multilateral development banks".8

Key achievements include:

- AA+ credit rating from S&P and Fitch

- RMB18 billion in Panda bonds issued

- Local currency lending in multiple BRICS currencies

However, limitations remain significant:

- Total lending capacity far below World Bank or Asian Development Bank

- Continued reliance on dollar markets for funding

- Limited project pipeline compared to established institutions

Payment Systems: Fragmentation vs Integration

Russia's SPFS and China's CIPS represent parallel attempts to create SWIFT alternatives. The Cambridge research details: "By the end of 2020, CIPS was processing RMB135.7 billion (USD19.4 billion) daily... More than 3,000 banks and other financial institutions have conducted actual business through CIPS".8

Yet fragmentation undermines effectiveness:

- Multiple incompatible systems (SPFS, CIPS, others)

- Limited international participation

- Continued reliance on SWIFT for global reach

The proposed BRICS Pay system aims to integrate national payment systems, but faces technical and political hurdles in creating true interoperability.

The Yuan Oil Futures: Market Innovation

China's yuan oil futures represent genuine market innovation. As the Cambridge analysis notes: "By the end of 2020, more than 83 percent of Russian exports to China were settled in euro... The euro has now replaced the US dollar and has become the primary vehicle currency in Russia-China trade".8

Market adoption shows gradual progress:

- Trading volumes surpassed Tokyo and Dubai

- Major energy companies using yuan settlement

- Gold convertibility option adds appeal

But context matters:

- Still fraction of London Brent or WTI volumes

- Limited to specific bilateral relationships

- Dollar pricing remains global standard

Media Patterns: Why Coverage Diverges

The Ideological Divide

Our analysis reveals that political ideology, more than economic evidence, drives de-dollarization coverage. Three distinct patterns emerge:

The Role of National Interest

The Chinese media paradox illustrates how national interest shapes coverage. Despite government promotion of de-dollarization, Chinese outlets score more moderately (2.90 propaganda risk) than Russian (1.85) or Iranian (2.15) media.

The Tricontinental piece by Gao Bai exemplifies this nuanced approach: "While they would prefer to have alternatives to the US dollar as the dominant currency, the dollar's depreciation would decrease the value of their large holdings of dollar-denominated assets".9

This reflects China's position as the largest foreign holder of US Treasuries at $784 billion. As the Cambridge analysis notes: "China remains embedded in an international financial system in which the US dollar is the key currency".8

This article scored 1 for both empirical evidence and citation quality, relying entirely on theory without a single data point.

Examining Exaggerated Claims

Our dataset reveals systematic patterns of misrepresentation though clear quality markers.

High-Quality Indicators:

- Multiple data sources (4.5+ empirical evidence)

- Acknowledgment of contradictory evidence

- Technical discussion of currency mechanics

- Historical context and precedents

- Diverse expert perspectives

Low-Quality Indicators:

- Government statements as primary sources

- Conflation of different de-dollarization types

- Absence of quantitative data

- Unsupported temporal predictions

- Single-perspective sourcing

Purely Opinion Pieces

While certain trends emerged, it is not simply that anti-Western media publications are solely responsible for a lack of empirical data. Certain mainstream banks and economic institutions are not always well-sourced either.

For example, a piece by Roman Kireev at the Mises Institute is largely ideological, presenting the theory that “the entire narrative of “de-dollarization” is not merely economically flawed, it is, at its core, a collectivist delusion,” without offering any meaningful analysis or supporting data.

The article takes jibes at traditional fiat currencies but positions USD as “tragically, the tallest dwarf in a monetary wasteland” and explains that “the language of “de-dollarization” conceals an authoritarian ambition: to replace one fiat empire with another. It is not a step toward sound money, but toward monetary nationalism. It is not liberation from the dollar; it is enslavement to a different tyrant.¹²

Using no sources or data whatsoever, the Mises Institute's analysis exemplifies ideological projection, scoring 1 on both empirical evidence and citation quality, and making sweeping claims about not just USD but fiat currencies as whole.

Statistical Manipulation

Russian sources pose statements like "83% of Russia-China trade is now in non-dollar currencies" without context. This impressive-sounding statistic obscures that Russia-China trade represents less than 1% of global commerce.

Similarly, claims about the Eurasian Economic Union (EAEU) de-dollarization being "almost complete" refer only to trade between Russia, Kazakhstan, Belarus, Armenia, and Kyrgyzstan, a tiny fraction of world trade.

Temporal Distortions

Iranian and Russian outlets consistently portray the dollar as rapidly losing global relevance, using evocative language. PressTV Iran's reporting that “sovereign countries, particularly BRICS members, are beginning to ditch the “toxic” dollar in order to “ensure their financial security”13 is clearly emotive, lacks specifics about non-BRICS countries reducing their dollar reliance, and fails to provide supporting data.

Quotes from the 10th Annual BRICS Parliamentary Forum were reported almost identically by Iran Press on the same day, 12 July 2024, suggesting a coordinated narrative. Both highlighted Volodin’s statement: 'Last year, its (the dollar’s) share in export-import transactions within the framework of the association was only 28.7%.”¹⁴ However, there is no further analysis of what proportion intra-BRICS trade represents in the context of global trade overall.

Scope Confusion

Many sources conflate:

- Bilateral trade arrangements with global currency shifts

- Political declarations with market realities

- Long-term possibilities with near-term probabilities

The Gradual Reality: What Credible Sources Say

Long-Term Evolution

The IMF-linked Funds Society analysis provides historical perspective: "Central banks have been gradually reducing their dollar holdings over the past couple of decades. USD as a share of forex reserves reached a 20-year low in late 2022 at 58 percent from a high of about 85 percent in the 1970s".15

This represents evolution, not revolution. J.P. Morgan adds: "While much of the reallocation of FX reserves has gone to CNY and other currencies, USD and EUR still dominate levels".¹

Structural Constraints

The Takshashila analysis clarifies fundamental limitations: "For a national currency to become a major world reserve currency, the home country must have a developed financial market, sufficient financial instruments available for investment, and capital account liberalization".⁷

These requirements explain why alternatives struggle:

- Yuan: Capital controls prevent full convertibility

- Euro: Fragmented bond markets limit depth

- Gold: Physical constraints and price volatility

- Cryptocurrencies: Regulatory uncertainty and instability

Network Effects

Even de-dollarization advocates acknowledge embedded advantages. Responsible Statecraft observes: "The dollar's deeply embedded infrastructure within financial markets and global trade, together with conflicting political goals amongst its detractors, suggests a practical replacement is unlikely".¹⁰

Key infrastructure includes:

- SWIFT processing 150 million messages daily

- Dollar invoicing in 40-50% of global trade

- $7.5 trillion daily forex market turnover

- Deep, liquid Treasury markets

The Technology Factor: Digital Currencies and Future Systems

Central Bank Digital Currencies

The Cambridge research details BRICS CBDC development: "China started its CBDC project in 2014 and revealed its strategic agenda in 2016... Russia's central bank outlined Russia's plan for a digital ruble, aiming to launch a pilot program at the end of 2021".⁸

Progress varies significantly:

- China: Digital yuan pilots in multiple cities

- Russia: Digital ruble in development

- Brazil: Targeted a 2022 launch (delayed)

- India: Research phase

- South Africa: Project Khokha testing

Only three countries have launched a CBDC: the Bahamas, Jamaica, and Nigeria.Yet CBDCs alone don't challenge dollar dominance, they digitise existing currencies without addressing fundamental reserve currency requirements.

Blockchain Payment Systems

By mid-2024, Project mBridge achieved its minimum viable product (MVP), marking a key milestone in its development. The initiative is designed to test a shared multi-central bank digital currency (CBDC) platform, allowing central and commercial banks from participating countries to carry out real-time cross-border payments and settlements using distributed ledger technology (DLT).

Benefits include:

- 24/7 operation

- Instant settlement

- Reduced counterparty risk

- Lower transaction costs

But scale remains limited compared to traditional systems processing trillions daily.

Economic Implications: Beyond the Headlines

For Developing Countries

The Responsible Statecraft analysis highlights genuine concerns: "For countries with large trade deficits with China, settling in RMB would not address their settlement cost concerns with the US dollar, and it actually would be more costly".¹⁰

Local currency settlement creates new risks:

- Exchange rate volatility

- Limited convertibility

- Accumulation of unusable currencies

- Reduced access to global markets

For the Global Financial System

The gradual shift toward multipolarity brings both opportunities and challenges:

Opportunities:

- Reduced single-point failure risk

- More monetary policy autonomy

- Regional financial deepening

- Innovation in payment systems

Challenges:

- Increased transaction costs

- Currency mismatch risks

- Fragmented liquidity pools

- Coordination difficulties

For the United States

J.P. Morgan's analysis suggests measured concern rather than alarm: "De-dollarization could shift the balance of power among countries, and this could, in turn, reshape the global economy and markets".¹

Potential impacts include:

- Gradual increase in borrowing costs

- Reduced "exorbitant privilege"

- Diminished sanctions effectiveness

- Need for fiscal discipline

Yet advantages remain substantial:

- Deep capital markets

- Rule of law

- Financial innovation

- Network effects

Looking Forward: Scenarios and Probabilities

Most Likely: Gradual Multipolar Evolution

Evidence points toward slow diversification rather than dramatic shifts. The dollar's share of reserves may decline from 59% to 45-50% over two decades, with multiple currencies gaining modest shares.

Supporting factors:

- Continued BRICS institution building

- Expanding local currency arrangements

- Technology enabling alternatives

- Growing emerging market weight

Less Likely: Accelerated De-dollarization

Rapid change would require catalytic events:

- Major US financial crisis

- Severe overuse of sanctions

- Technological breakthrough

- Coordinated alternative system

Even then, transition costs and network effects create substantial inertia.

Key Takeaways

Conclusion

The de-dollarization narrative reveals as much about information quality as monetary economics. Dollar dominance will likely erode gradually over coming decades, not through dramatic collapse but through the natural evolution of a multipolar global economy. Payment technologies will advance, emerging markets will grow, and the US may inadvertently undermine dollar strength through fiscal policies and sanctions overreach.

Our analysis offers a simple framework for evaluating de-dollarization claims: the inverse relationship between certainty and credibility. Sources expressing absolute certainty about timelines and outcomes consistently score lowest on evidence quality. Conversely, those acknowledging uncertainty while tracking concrete developments provide the most valuable insights.

For those navigating this complex landscape, focus on sources scoring above 3.5 on our propaganda risk index. They may lack the dramatic headlines, but they offer something more valuable: accurate analysis grounded in evidence rather than ideology.

The international monetary system continues to evolve, as it always has. Understanding this evolution requires separating signal from noise, evidence from propaganda, and gradual change from revolutionary rhetoric. In this task, media literacy becomes as important as financial literacy.

Sources

- J.P. Morgan Global Research. "De-dollarization: Is the dollar losing its dominance?" J.P. Morgan, June 3, 2024. https://www.jpmorgan.com/insights/global-research/currencies/de-dollarization

- Engels, Janet & Cooper, Laura. "De-dollarization: The dollar in doubt." RBC Wealth Management, April 29, 2024. https://www.rbcwealthmanagement.com/en-us/insights/de-dollarization-the-dollar-in-doubt

- Wade, Robert H. "Long Read: The beginning of the end for the US dollar's global dominance." LSE International Development Blog, February 29, 2024. https://blogs.lse.ac.uk/internationaldevelopment/2024/02/29/long-read-the-beginning-of-the-end-for-the-us-dollars-global-dominance/

- Tasnim News Agency. "De-Dollarization Process Led by Russia Almost Complete: Report." Tasnim News, February 3, 2024. https://www.tasnimnews.com/en/news/2024/02/03/3033217/de-dollarization-process-led-by-russia-almost-complete-report

- Durden, Tyler. "Dollar's Decline Meets Rising Dedollarization: The Threat Comes From Within." ZeroHedge, June 23, 2025. https://www.zerohedge.com/geopolitical/dollars-decline-meets-rising-dedollarization-threat-comes-within

- Feng, John. "Donald Trump Warns BRICS Over Dollar Move: 'Go Find Another Sucker Nation'." Newsweek, January 31, 2025. https://www.newsweek.com/brics-dollar-donald-trump-tariffs-2024004

- Manur, Anupam. "De-dollarisation: Temporary blip, prolonged dip, or inevitable demise?" Takshashila Discussion Document No. 2024-12, July 2024. https://takshashila.org.in/research/de-dollarisation-discussion-doc

- Liu, Z. & Papa, M. (eds). "Can BRICS De-dollarize the Global Financial System?" Cambridge University Press, February 2, 2022. https://www.cambridge.org/core/books/can-brics-dedollarize-the-global-financial-system/0AEF98D2F232072409E9556620AE09B0

- Bai, Gao. "From De-Risking to De-Dollarisation: The BRICS Currency and the Future of the International Financial Order." The Tricontinental, October 2023. https://thetricontinental.org/wenhua-zongheng-2024-1-derisking-dedollarisation-brics-currency/

- Responsible Statecraft Staff. "De-dollarization not a matter of if, but when." Responsible Statecraft, May 3, 2023. https://responsiblestatecraft.org/2023/05/03/de-dollarization-not-a-matter-of-if-but-when/

- Norton, Ben. "Trump's tariffs turbocharge de-dollarization: World sells US dollar assets, seeking alternatives." Geopolitical Economy Report, May 5, 2025. https://geopoliticaleconomy.com/2025/05/05/trump-tariffs-dedollarization-sell-us-dollar/

- Kireev, Roman. "The Delusion of De-Dollarization." Mises Institute, July 1, 2023. https://mises.org/power-market/delusion-de-dollarization

- Press TV Staff. “'US Sanctions backfired': De-dollarization tops agenda of BRICS Parliamentary Forum”. Press TV Iran, July 12 2024. https://www.presstv.ir/Detail/2024/07/12/729179/De-dollarization-agenda-BRICS-Parliamentary-Forum-

- Iran Press/Europe. "'De-dollarization tops agenda of BRICS Parliamentary Forum." Iran Press, July 12, 2024. https://iranpress.com/content/284145/de-dollarization-tops-brics-parliamentary-forum-agenda

- Funds Society Staff. "Central banks are gradually moving away from the dollar, but the process will be very slow." Funds Society, June 26, 2024. https://www.fundssociety.com/en/news/markets/central-banks-are-gradually-moving-away-from-the-dollar-but-the-process-will-be-very-slow/